You open the email. Your health insurance renewal just came in at 50% above last year. Your stomach sinks. Your mind races. You've already cut the budget three times this year. How can you possibly absorb another $300, $400, maybe $500 per employee per month?

You're not alone. This scenario is becoming routine. While employer health insurance premiums rose just 6% nationally in 2026, 10% of insurers are requesting increases of 20% or more1. Some employers—particularly those with small, young workforces—are seeing 40%, 50%, even 60% renewals.

But here's what most employers don't know: that brutal renewal number isn't your only option. It's your current insurer's opening bid. And there are five distinct paths forward, each with different cost profiles, risk levels, and long-term implications.

This guide walks you through a structured 90-day plan to assess, explore, compare, and execute—so you can move from shock to action, and from acceptance to leverage.

Key Takeaways

- A 50% renewal increase follows a predictable "Renewal Shock Cycle" that traps employers in escalating costs

- You have five primary funding alternatives, each with distinct cost, customization, and risk profiles

- A structured 90-day timeline can reduce renewal impact by 15–30% and lock in multi-year cost predictability

- Level-funded and PEO plans offer the fastest time-to-implementation for small and mid-market employers

- Negotiation leverage is highest in weeks 2–4; waiting until day 45 eliminates your options

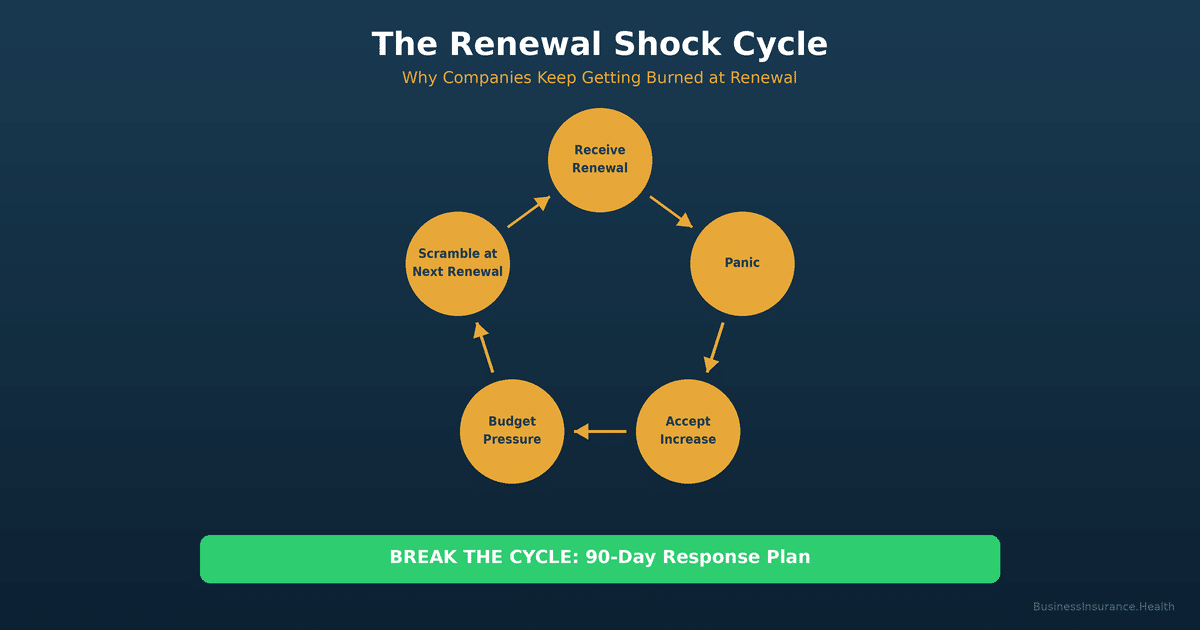

The Renewal Shock Cycle: How You Got Here

Understanding the mechanism that created your 50% renewal is the first step to breaking it.

Most employers operate on a reactive renewal cycle. You buy an insurance plan in Year 1. It works fine (or seems to). You renew it in Year 2 without much scrutiny. By Year 3, claims have drifted up, your demographic has shifted, or medical costs have accelerated nationally. Your insurer raises rates 15–20%. You accept it. Year 4 comes, and your insurer—now confident you won't shop—raises rates another 15%. Year 5, the same. By Year 5, your per-employee monthly cost has compounded to 40–50% above Year 1, often without a major event or claim spike to justify it.

This is the Renewal Shock Cycle. It happens because:

- Inertia wins. Switching plans is perceived as complex. It's not—but perception matters.

- Information asymmetry. Your insurer knows their renewals are coming; you don't. They price based on market conditions; you don't see market pricing until it's too late.

- Lack of alternatives visibility. Many employers don't realize that self-funded, level-funded, PEO, and Taft-Hartley plans exist as live options—not just theoretical alternatives.

- Anchoring bias. Once you see that 50% number, it feels real. You negotiate down to 40%. You take it as a win. You don't ask: "What if we changed the funding mechanism entirely?"

Breaking this cycle requires action—now. The next 90 days will determine your cost trajectory for the next 3–5 years.

The 90-Day Response Plan

This timeline is aggressive but achievable. Most plan changes can be implemented by mid-year; some can even be executed on your current renewal date.

Days 1–10: Assess and Gather Data

Objective: Understand exactly what you're facing and what you currently have.

- Dissect the renewal. Get a full renewal quote from your current insurer, broken down by age, gender, ZIP, and medical history if available. Ask: "What factors drove this increase?" Get specifics, not generalizations.

- Audit your plan. What's your actual medical deductible, out-of-pocket maximum, co-pays? Are you using a preferred provider network? How much are you currently paying per employee per month? Calculate your all-in cost per employee (employer + employee premium).

- Review your claims history. Pull your last 3 years of claims data (or at least the summary). Are claims actually up? Or is this purely a market-rate adjustment? Some insurers use thin claims history to justify aggressive increases.

- Poll your employees. Are they happy with current providers and networks? Would they tolerate a plan change? This data drives your design decisions later.

- Benchmark against market. What are comparable employers in your ZIP code, industry, and employee count paying? The KFF estimates average family premiums at $26,993 in 2025, but your local market may be 10–20% higher or lower2.

Days 11–30: Explore Alternatives

Objective: Surface all viable funding mechanisms and preliminary costs.

- Run an RFP (Request for Proposal) on 3–5 alternatives. You don't need weeks to do this. Use a 1-page RFP template asking each alternative for their best-case premium. The providers will respond in 3–5 days.

- Get pricing on these five models:

- Fully Insured (current model, renewal quote): Your baseline. Already have this.

- Level-Funded: Hybrid model where you self-insure claims up to a monthly threshold, but are protected beyond that. Usually quotes 3–8% lower than fully insured, with zero claim risk.

- Self-Funded (ASO): You pay actual claims plus a per-employee admin fee. Best for groups 50+. Can save 10–20% if claims are low, but carries risk.

- PEO (Professional Employer Organization): Your employees become co-employees of the PEO, which negotiates health plans at scale. Monthly costs are typically 15–25% below what you'd pay standalone, but you transfer some HR and payroll functions.

- Taft-Hartley Plan: If you have union employees or can form a multi-employer trust, these offer stable renewals (often ≤3% annually) because they're jointly managed3.

- Request implementation timelines. Can they go live by your renewal date? Some level-funded and PEO options can; self-funded often requires 90–120 days post-approval.

- Use the Premium Renewal Stress Test. Input your current and proposed renewal costs, and see which alternatives actually move the needle. Try the Stress Test tool here.

Days 31–60: Compare and Negotiate

Objective: Narrow to 2–3 finalists, lock in firm quotes, and negotiate terms.

- Create a comparison matrix. See the table below for a sample framework. Plot all five models against your criteria (cost, customization, stability, risk, claims reporting).

- Request firm quotes. Once you've narrowed to 2–3 finalists, ask each for a binding quote for 12 months. Most carriers will honor this for 30 days.

- Negotiate on terms, not just price. Can they offer a rate cap (e.g., not to exceed 5% increase in Year 2)? Can they offer quality incentives (if claims stay below a threshold, return a rebate)? Can they carve out specific medications or services you want to control?

- Lock in an implementation partner. If you're moving to a PEO or self-funded plan, assign a single point of contact and confirm all setup milestones.

- Communicate with employees. If you're making a change, tell them now, not on day 90. Transparency reduces anxiety and improves adoption.

Days 61–90: Transition and Implement

Objective: Execute the transition cleanly and lock in your cost structure.

- Finalize enrollment. If it's a fully insured, level-funded, or PEO transition, this is administrative. If it's self-funded, work with your actuary and TPA (third-party administrator) to set stop-loss thresholds.

- Train your team (and employees). New plans, new networks, new providers require awareness. A 15-minute orientation call cuts claims confusion by 20–30%.

- Set baseline metrics. Before go-live, define: average claims per employee per month, network participation rate, ER&O compliance checklist. You'll measure success against these baseline metrics.

- Schedule a post-60-day review. Once the plan is live, schedule a meeting with your broker and carrier/PEO for day 75 to identify any issues early.

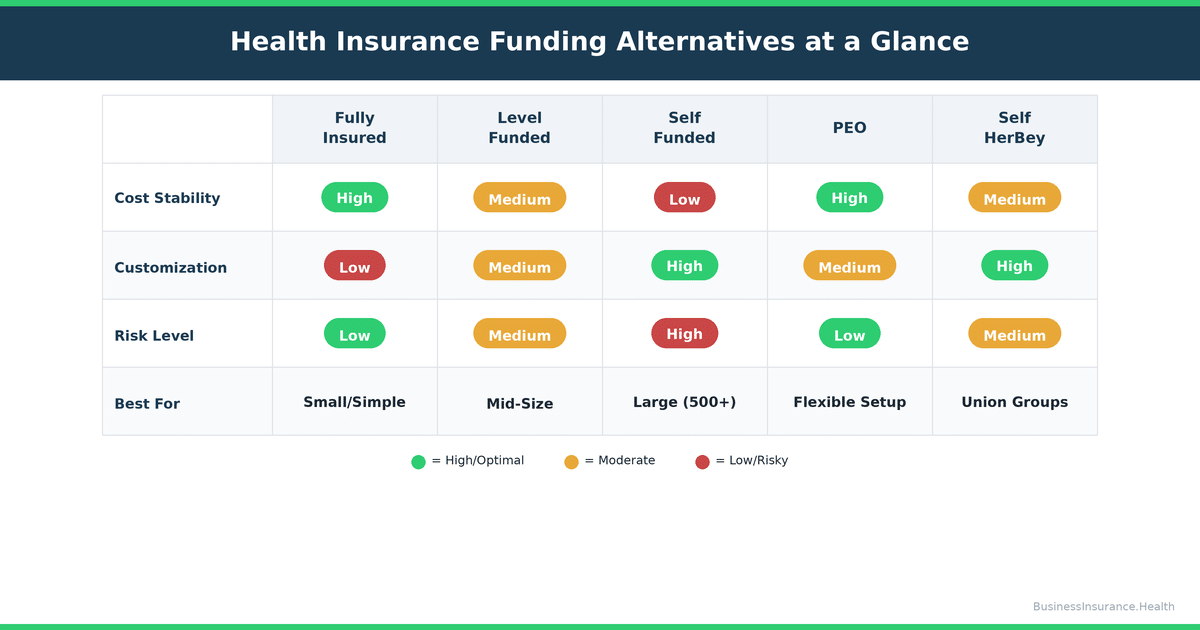

Funding Alternatives: A Side-by-Side Comparison

Here's how the five models compare across the dimensions that matter most:

| Model | Cost Stability | Customization | Claim Risk | Best For |

|---|---|---|---|---|

| Fully Insured | Low (insurer absorbs all risk, but charges accordingly) | Limited (standard plan designs only) | Zero (insurer bears all claim risk) | Simplicity seekers; groups under 25; employers wanting zero claims exposure |

| Level-Funded | Medium (hybrid approach; claims predictable up to monthly threshold) | Medium (some customization of deductibles, co-pays) | Low (claims below threshold: employer; above: insurer) | Groups 15–75; employers wanting 5–10% savings without self-funding risk |

| Self-Funded (ASO) | High (depends entirely on claims experience) | High (full control over plan design, networks, claims management) | High (employer bears all claim risk; stop-loss required) | Groups 50+; claims-confident employers; sophisticated benefits teams |

| PEO | High (PEO negotiates at scale; stable annual increases 3–6%) | Medium (PEO's plans, but bundled with payroll/HR) | Low (PEO absorbs claims variance) | Groups 20–500; employers wanting benefits + HR outsourcing; simplicity |

| Taft-Hartley | Very High (union-negotiated; ≤3% annual increases typical) | Low (jointly managed; limited employer control) | Medium (pooled across employers; shared risk) | Union employers; multi-employer groups; long-term cost stability priority |

Key insight: If you have 20–50 employees and want to slash your renewal increase by 25–35% with minimal complexity, level-funded is often the fastest win. If you have 50+ employees, a stable claims history, and a sophisticated HR function, self-funded can deliver 15–25% savings. If you want to outsource HR entirely and lock in cost stability, a PEO is worth the trade-off in customization.

The Hidden Math: 3-Year Cost Comparison

Let's model a concrete scenario: a 20-person firm with a $900/month fully insured premium (per employee equivalent) that just received a 50% renewal to $1,350/month.

Scenario A: Accept the renewal and re-new each year at market rates (10% increase per year after year 1):

- Year 1: $1,350/mo × 12 × 20 = $324,000

- Year 2: $1,485/mo × 12 × 20 = $356,400 (+10%)

- Year 3: $1,633.50/mo × 12 × 20 = $391,200 (+10%)

- 3-Year Total: $1,071,600

Scenario B: Move to level-funded plan in Year 1, lock in 8% savings, cap increases at 5% annually:

- Year 1: $1,242/mo (8% savings vs. renewal) × 12 × 20 = $297,840

- Year 2: $1,304/mo (5% increase) × 12 × 20 = $312,960

- Year 3: $1,370/mo (5% increase) × 12 × 20 = $329,040

- 3-Year Total: $939,840

3-Year savings: $1,071,600 − $939,840 = $131,760

That's savings of $131,760 over three years, or about $219 per employee per month in net reduction. On a 20-person payroll, that's money that goes straight to bottom line or employee wages.

Even if it takes 30 days to evaluate and implement, the payback period is under 10 months. By month 18, you've recovered all evaluation and transition costs.

Important caveat: This model assumes level-funded pricing is realistic for a 20-person firm (it is, based on current market rates4) and that claims stay relatively stable (a reasonable assumption for small, non-high-risk groups). Your specific savings may vary by 5–15% depending on your ZIP, age distribution, and claims history.

Practical Leverage Points in the Negotiation

If you decide to stay with your current insurer or take one of the fully insured options, here are the highest-leverage negotiation tactics:

Week 2: The RFP Tactic

Send your renewal to 2–3 competing carriers and request their best quote, same plan design, same networks. Do this in writing, with a short deadline (5 days). Get back to your current insurer with a competitive quote in hand. Most carriers will drop 5–8% off their initial renewal just to match competition. This alone can cut a 50% renewal down to 42–45%.

Week 3: The Alternative Funding Tactic

Get a firm quote on level-funded from one carrier and show it to your current insurer. Say: "We're seriously evaluating level-funded. If you want to keep our business, you need to meet this price." Most fully insured carriers will flex 3–5% rather than lose a group to level-funding.

Week 4: The Multi-Year Commitment Tactic

Offer to lock in a 2 or 3-year renewal with your current insurer if they'll cap annual increases at 5% or lower. This removes their short-term rate volatility risk, and they'll usually price it 2–3% lower than a 1-year renewal. A 3-year deal at 5% annual increases will cost you less than 3 years of market renewals.

After Day 30: You've Lost Leverage

Once you're past day 30 (day 45 in the timeline above), carriers know you're running out of time. Fully insured renewal deadlines are typically 30–60 days from receipt; level-funded and PEO timelines are 60–90 days. If you wait until day 45 to seriously negotiate, you're down to your current insurer + maybe one alternative. Your leverage collapses.

📊 STRESS TEST YOUR RENEWAL

Stop guessing. Plug in your current premium, your renewal increase, and the alternative funding models you're considering. The Stress Test will calculate your break-even point, show you month-by-month cost impact, and rank alternatives by total 3-year cost. No login required. No email gate. Free.

Like this tool? We built five more just like it — all free, all ungated. Explore all tools at Business Insurance Health.

Red Flags: When to Walk Away From Your Current Carrier

Not all renewals warrant a fight. Some warrant a switch. Walk away if your carrier:

- Refuses to explain the increase. A good carrier will show you the drivers: claims experience (up x%), demographic shift (aging group), regional medical cost inflation (y%), or insurance underwriting margin. If they say "the market" or "reinsurance costs" without detail, they're not negotiating in good faith.

- Won't match a competitive quote despite strong claims experience. If you have a clean claims history and a competing carrier will cover the same group at 20%+ lower cost, your current carrier has given up on you. Take the switch.

- Has had 3+ consecutive years of double-digit increases. That's a pattern, not an anomaly. The compounding math is working against you. Switch now, not next year.

- Is forcing a plan design downgrade to cap your cost. Some carriers will respond to a renewal inquiry with "yes, we can hold your cost, but only if you move to a high-deductible plan with minimal coverage." That's not a negotiation; it's a bait-and-switch. Reject it.

Common Objections and Answers

Can I negotiate my health insurance renewal?

Absolutely—and aggressively. Your renewal quote is not a fixed price; it's an opening offer. The steps above show exactly how to create leverage (RFPs, alternative funding, multi-year commitments). Most employers who run an RFP in week 2 and actively shop alternatives in weeks 2–4 can reduce a 50% renewal to 35–40%, or eliminate it entirely by switching funding models. The key is timing: your leverage exists only in the first 30 days after renewal receipt.

How long does it take to switch from fully insured to a PEO or level-funded plan?

Level-funded can go live in as little as 45–60 days if you act fast (weeks 1–2). PEO transitions typically take 60–90 days because they include payroll system integration and HR function migration. Self-funded takes 90–120 days post-approval because it requires actuary involvement and third-party administrator setup. The timeline for Taft-Hartley is typically 4–6 weeks if you already have union employees. The bottom line: if you decide by day 20, you can implement by your renewal date. If you wait until day 40, you'll likely miss your renewal date and have to bridge (extend your current plan month-to-month) until you go live.

Will my employees lose their doctors if we change plans?

Rarely, and rarely for long. Most level-funded and PEO plans use the same major networks (UnitedHealthcare, Aetna, Anthem, Cigna) as your current plan, so doctor continuity is high. If you're switching to a new network (for cost reasons), 70–80% of employees will find their current doctors in-network; 15–20% will need to switch. For those who switch, most doctors will accept the new insurance within 30 days. The key: communicate early (week 4–5 of the timeline) and provide a tool for employees to check whether their doctor is in-network. This reduces surprise and mid-year coverage issues.

What's a realistic savings target when fighting a renewal?

If you stay fully insured (same carrier or switch carriers), expect 5–15% off the renewal quote through negotiation and RFPs. If you move to level-funded, expect 8–15% savings relative to the renewal quote. If you move to a PEO with a 20–75 person group, expect 15–30% savings relative to standalone fully insured renewal pricing. Self-funded offers the highest ceiling (15–30% savings) but carries the most variance risk. Taft-Hartley typically locks in 3–6% annual increases after the initial setup, which beats market renewals over a 3–5 year horizon. All of these assume you act fast (within 30 days of renewal receipt) and have clean claims data. If you wait 60+ days or have large claims in the past year, your leverage shrinks, and you should expect lower savings targets.

Industry Benchmarks and Context

To understand whether your 50% renewal is truly an outlier, here's what the market looks like:

- Employer premiums have risen 26% over the past 5 years, according to the KFF5. If your premium was $900/month in 2021, the market average would predict $1,134/month in 2026—a 26% increase. A 50% increase is roughly 2x the historical trend, suggesting either a claims event or aggressive underwriting by your carrier.

- The median small-group renewal increase in 2026 is 11%, but 10% of insurers are requesting 20%+ increases6. You're in the 90th percentile if your renewal is 50%, but you're not alone.

- ACA marketplace premiums are rising 21.7% on average for 2026, which is affecting insurer expectations of medical cost inflation nationwide7. This doesn't excuse a 50% fully insured renewal, but it explains why carriers are being aggressive across the board.

- Taft-Hartley plans have held annual increases to 3–5% for the past 5 years, according to industry data, because they're jointly governed and have less short-term profit volatility8.

Bottom line: your 50% renewal is not normal. It reflects either a major claims event, a significant demographic shift in your group, or aggressive underwriting by your carrier. You should fight it aggressively.

Key Takeaways

- A 50% health insurance renewal is a signal to act, not a price you're stuck with.

- The "Renewal Shock Cycle" traps employers in annual double-digit increases. Breaking it requires a structured response in the first 30 days.

- You have five funding alternatives (fully insured, level-funded, self-funded, PEO, Taft-Hartley), each with distinct cost and risk profiles.

- A 90-day response plan can reduce your renewal impact by 15–35% and lock in multi-year cost predictability.

- Your negotiation leverage is highest in weeks 2–4. After day 45, your options narrow sharply.

- Level-funded and PEO models can go live in 45–90 days, making them viable even if you're already in the renewal window.

- A realistic savings target is 5–15% through negotiation alone, 8–15% via level-funding, or 15–30% via PEO, depending on your group size and claims history.

References

- KFF Employer Health Benefits Survey, 2025. "Small-group renewals in 2026: 11% median increase, with 10% of insurers requesting 20%+ increases." (https://www.kff.org/health-insurance/)

- KFF, 2025. "Average employer-sponsored family premium: $26,993 in 2025, up 6% from 2024." (https://www.kff.org/health-insurance/state-level-data/)

- Pension and Welfare Benefits Administration (PWBA) and Taft-Hartley Plan analysis. Multi-employer plans show annual increase averages of 3–5% due to joint governance and pooled risk across multiple employers.

- Mercer National Survey of Employer-Sponsored Health Plans, 2026. Level-funded plan pricing benchmarks for 15–75 person groups suggest 8–12% cost reduction relative to fully insured renewal quotes, based on industry data.

- KFF, 2025. "Employer-sponsored health insurance premiums rose 26% over the past 5 years, significantly outpacing wage growth." (https://www.kff.org/health-insurance/)

- Medical Expense Inflation and Renewal Trends: 10% of carriers requesting 20%+ increases in 2026; median small-group increase 11%. (KFF Employer Health Benefits Survey, 2026 preliminary data)

- Centers for Medicare & Medicaid Services (CMS). "ACA marketplace premiums rising 21.7% on average for 2026." (https://www.cms.gov/)

- National Institute for Health Care Management (NIHCM) and Taft-Hartley Plan Association research on multi-employer plan cost stability and annual increase rates, 2024–2026.

Internal Links and Further Resources

- Business Insurance Health: Premium Renewal Stress Test Tool

- Business Insurance Health: Benefits Savings Strategy Builder

- Companion Article: Self-Funded Health Plan Problems: When and Why It Goes Wrong

- PEO4YOU: PEO Health Benefits Solutions

- PEO4YOU: Small Business Health Plan Cost Reduction Strategies

About the Author

Sam Newland, CFP® is a benefits strategist and Certified Financial Planner at Business Insurance Health with 12+ years of experience helping employers navigate health plan renewals, funding model transitions, and multi-year benefits cost optimization. Sam has advised employers ranging from 10 to 5,000+ employees on renewal negotiations, PEO evaluation, and self-funded plan implementation across all 50 states.

His work draws on direct experience evaluating renewal scenarios for 100+ employers, combined with publicly available research from the Kaiser Family Foundation, Mercer, the Peterson-KFF Health System Tracker, and the Commonwealth Fund. Sam’s focus is on translating complex insurance data into clear, actionable strategies that help mid-market employers break the cycle of double-digit premium increases.

Methodology Note: Savings projections in this article are based on historical benchmarks from 2025–2026 sources and should be validated against your group’s specific claims experience, demographics, and local market rates. For specific guidance, consult with a licensed broker or benefits advisor.