Your CFO just asked a question that is becoming increasingly common in benefits strategy meetings: “Why are we picking one health plan for everyone when our employees have completely different needs?”

It is a fair question. A 28-year-old software developer and a 58-year-old operations manager have wildly different health care needs, risk profiles, and coverage preferences. Yet traditional group coverage forces both onto the same plan — or at best, offers two to three options that satisfy neither perfectly.

Enter the Individual Coverage Health Reimbursement Arrangement (ICHRA) — a benefits model where the employer contributes a defined dollar amount and employees choose their own individual market plan. ICHRA adoption grew 34% among large employers and 18% among small employers from 2024 to 2025, according to the HRA Council.1 That growth is accelerating into 2026, with the 18-44 age group comprising over 50% of ICHRA enrollees, strengthening risk pools and driving long-term affordability.7

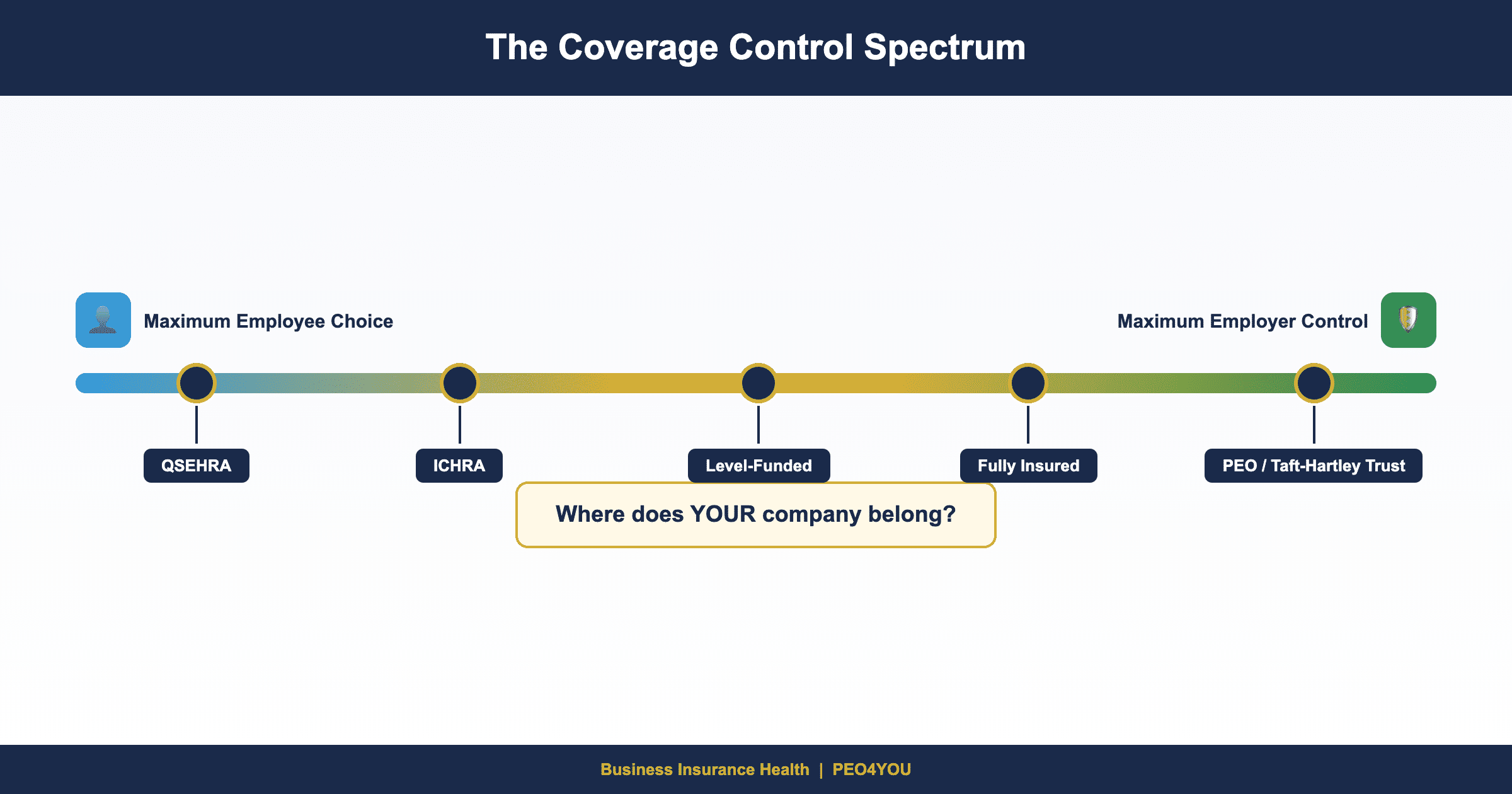

But ICHRA is not the right answer for every company. At Business Insurance Health and PEO4YOU, we evaluate both strategies against what we call The Coverage Control Spectrum — a framework for determining whether your company benefits more from controlled group coverage or defined-contribution flexibility.

Key Takeaways

- ICHRA adoption grew 34% among large employers and 18% among small employers from 2024 to 2025 — the fastest-growing benefits model in the market.1

- ICHRA has no minimum or maximum employer contribution limit, giving employers complete budget control while employees choose plans tailored to their needs.2

- Group coverage (including PEO and Taft-Hartley trust plans) offers lower deductibles, pooled risk protection, and claims advocacy that ICHRA employees navigating the individual market do not receive.

- The decision depends on workforce demographics: companies with diverse age ranges and geographic spread may benefit from ICHRA’s flexibility; companies with concentrated workforces often get better value from pooled group coverage.

- Hybrid approaches are emerging: some employers offer group coverage for full-time core staff and ICHRA for part-time, seasonal, or remote workers in different states.

The Coverage Control Spectrum: Two Fundamentally Different Approaches

Every employer benefits strategy falls somewhere on The Coverage Control Spectrum:

| Dimension | ICHRA (Defined Contribution) | Group Coverage (Defined Benefit) |

|---|---|---|

| Employer control | Budget only — employees choose plans | Plan design + carrier + network |

| Employee choice | Maximum — any ACA-compliant plan | Limited to plans employer selects |

| Budget predictability | Fixed — employer sets contribution | Variable — renewals change annually |

| Deductible levels | Depends on employee plan choice | Employer controls (often $1K–$3K) |

| Claims advocacy | None — employee navigates alone | PEO/broker intervenes on disputes |

| Risk pooling | Individual market (no pooling) | Pooled (trust or large group) |

| Multi-state coverage | Employees buy local plans | National PPO or multi-state access |

| ACA compliance | Satisfies employer mandate if affordable3 | Satisfies employer mandate |

| Contribution limits | No min or max2 | Market-driven premiums |

| Best for | Distributed, diverse workforce | Concentrated workforce wanting rich plans |

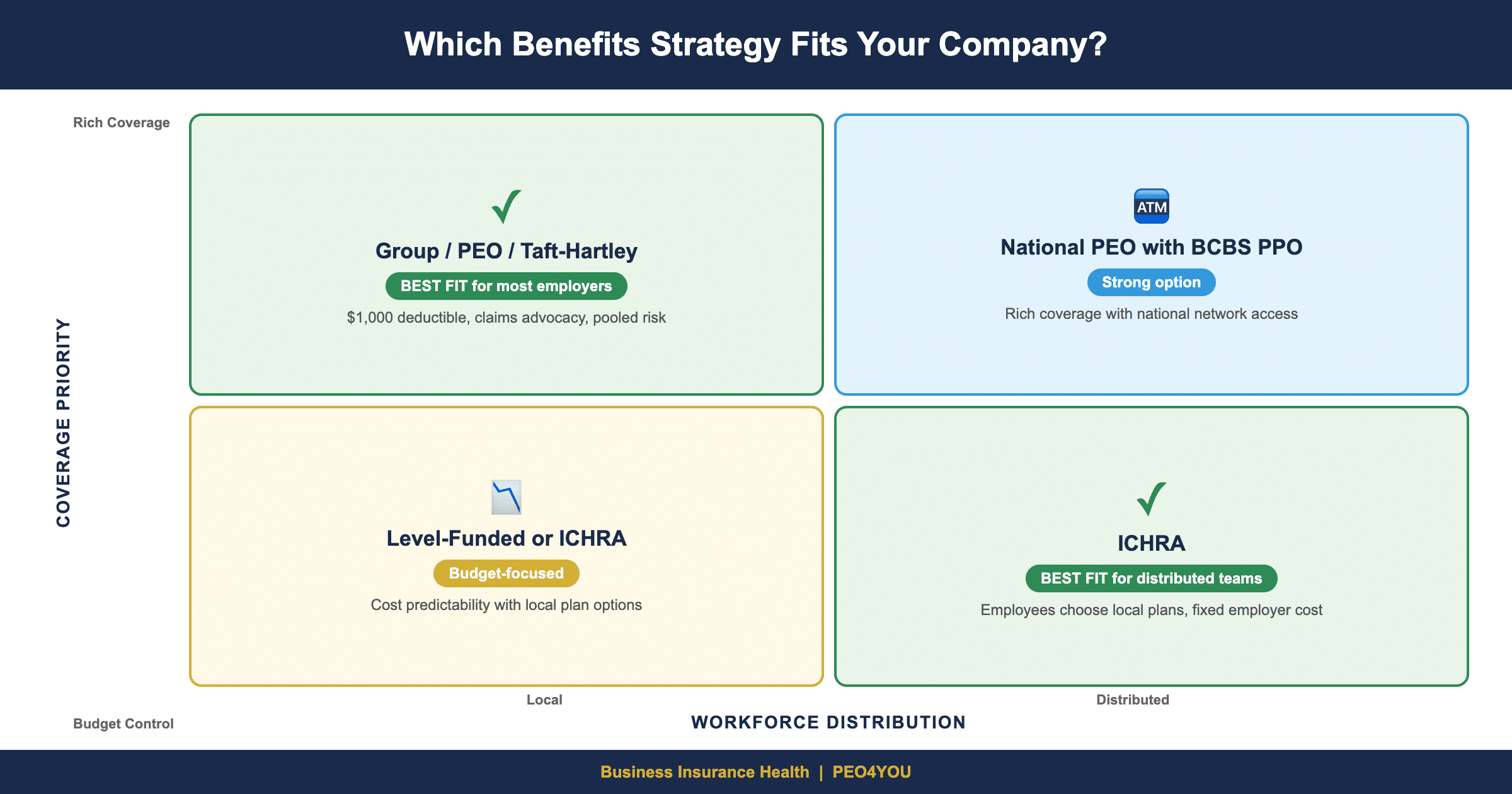

When ICHRA Makes Sense

ICHRA works best in specific scenarios:

1. Geographically Distributed Teams

If you have employees in 10 states, finding a single group plan with adequate network coverage in all 10 is nearly impossible. With ICHRA, each employee buys a plan with a strong local network in their area. The employer contributes the same amount regardless of location.

2. Diverse Workforce Demographics

A company where employee ages range from 25 to 64 may find that a single group plan overserves some and underserves others. ICHRA lets the 25-year-old choose a lower-cost HDHP while the 60-year-old selects a richer PPO — both funded by the same employer contribution.

3. Budget Certainty Is the Priority

With group coverage, renewal increases of 7% to 19% are annual surprises. ICHRA contributions are fixed by the employer — you set the budget, and it does not change until you decide to change it. With employer health costs projected to exceed $17,000 per employee in 2026 according to Aon,4 that predictability has real value.

4. Companies Under 50 Employees (No ACA Mandate)

Companies not subject to the ACA employer mandate have more flexibility. ICHRA allows them to provide a meaningful benefit without the complexity and cost of establishing a group plan. The employer sets a monthly allowance (there is no minimum), and employees buy individual market coverage.

When Group Coverage Wins

1. Plan Quality Matters More Than Flexibility

A Taft-Hartley multiemployer trust through PEO4YOU delivers a $1,000 deductible, $3,800 OOP max, and first-dollar copays — plan designs that do not exist in the individual market at comparable prices. If your employees value rich coverage over plan choice, group wins.

2. Claims Advocacy Is Non-Negotiable

When an ICHRA employee has a claim denied on their individual market plan, they are on their own. There is no PEO benefits specialist to call. There is no institutional leverage with the carrier. With some major carriers denying 20% to 25% of claims (per CMS PY2024 data),5 this is not a theoretical concern — it is a near-certainty for any employee with significant medical utilization.

3. Retention Through Benefits Is Strategic

An employee receiving a $47/month share of a $1,000 deductible BCBS PPO plan is materially harder to recruit away than an employee receiving a $500/month ICHRA reimbursement who still faces a $2,789 average marketplace deductible.6 The group plan creates a retention moat; the ICHRA creates a benefit that can be replicated by any employer.

4. You Have a Concentrated Local Workforce

If most of your employees are in one metro area, a group plan with a strong local network provides better coverage at lower cost than individual market plans. The pooled risk advantage outweighs the flexibility advantage when geography is concentrated.

The Hybrid Approach: ICHRA + Group Coverage

An emerging strategy that we are implementing at Business Insurance Health for select clients: offer group coverage for core full-time employees and ICHRA for specific employee classes where flexibility matters more.

Under IRS rules, employers can offer ICHRA to certain employee classes while maintaining group coverage for others, as long as the classes are defined by objective criteria (full-time vs. part-time, salaried vs. hourly, geographic location, etc.).3 You cannot offer both ICHRA and group coverage to the same employee class.

Example structure:

- Full-time headquarters staff (25 employees): PEO group coverage through Taft-Hartley trust — $1,000 deductible, BCBS PPO, claims advocacy

- Remote workers in 5 states (10 employees): ICHRA at $500/month — employees buy local plans with strong regional networks

- Part-time workers (8 employees): ICHRA at $250/month — meaningful contribution without the cost of group coverage

This hybrid approach gives each employee class the coverage model that works best for their situation while keeping the employer’s total benefits budget controlled and predictable.

For more on how PEO group coverage compares on cost, see PEO cost analysis and for the tax advantages of structuring contributions pre-tax, see Section 125 cafeteria plan FICA savings at PEO4YOU.

📊 CALCULATE YOUR BENEFITS ROI

Compare the return on investment across ICHRA, group, and PEO coverage models. Use the Benefits ROI Calculator below — no login required, no email gate, free.

Frequently Asked Questions

Does ICHRA satisfy the ACA employer mandate for companies with 50+ employees?

Yes, if the ICHRA contribution meets the affordability threshold — the employee’s lowest-cost silver plan premium minus the ICHRA contribution must not exceed 9.96% of household income (2026 threshold). Employers must determine affordability using one of the IRS safe harbors (W-2, rate of pay, or federal poverty line). If the ICHRA is not affordable, the employee can decline it and access marketplace subsidies instead.3

Can employees keep marketplace subsidies if they have an ICHRA?

No — if an employee is offered an affordable ICHRA, they are not eligible for marketplace premium tax credits. However, an employee can decline an unaffordable ICHRA and access subsidies. This is a critical design consideration: set ICHRA contributions too low, and employees may be better off declining the ICHRA and keeping their subsidies.2

Is there a minimum or maximum ICHRA contribution?

No. Unlike QSEHRA (which has IRS-set maximums of $6,450 individual / $13,100 family in 2026), ICHRA has no contribution limits. Employers can contribute $100/month or $2,000/month — the amount is entirely at the employer’s discretion.2

Can we offer ICHRA to some employees and group coverage to others?

Yes, as long as employee classes are defined by objective, IRS-approved criteria. You cannot offer both to the same class, and the classes must be based on bona fide employment criteria (full-time/part-time, salaried/hourly, geographic location, etc.), not individual employee characteristics.3

How does ICHRA compare to QSEHRA for small employers?

QSEHRA is simpler but limited: it is only available to employers with fewer than 50 employees who do not offer group coverage, and it has annual contribution maximums. ICHRA has no size restriction, no contribution limits, and can be offered alongside group coverage (to different employee classes). For employers over 50 employees or those wanting higher contribution amounts, ICHRA is the more flexible option.

📊 BENCHMARK YOUR PLAN QUALITY

Plan Quality & HRA Analyzer at businessinsurance.health

Compare your current coverage structure — whether ICHRA, group, or hybrid — against institutional benchmarks. See how deductible levels, networks, and total costs stack up.

No login required. No email gate. Free.

References

- HRA Council / healthinsurance.org. “ICHRA Adoption Trends 2024-2025.” January 2026. healthinsurance.org. Large employer ICHRA adoption grew 34%; small employer grew 18%.

- PeopleKeep. “Guide to the Individual Coverage HRA (ICHRA) for 2026.” peoplekeep.com. “The ICHRA has no minimum or maximum employer contribution limits.”

- Internal Revenue Service. “Individual Coverage Health Reimbursement Arrangements.” irs.gov. Employee class rules, affordability requirements, ACA mandate compliance.

- Aon plc. “U.S. Employer Health Care Costs Expected to Rise 9.5 Percent in 2026.” September 2025. aon.mediaroom.com.

- Muni Health / CMS Transparency in Coverage Data. “Claims Denial Rates by Insurer 2026.” March 2026. muni.health.

- Peterson-KFF Health System Tracker. “ACA Marketplace Average Deductible.” November 2025. healthsystemtracker.org. Average individual market deductible: $2,789.

- Henderson Brothers. “ICHRA Update — Looking Ahead to 2026.” August 2025. hendersonbrothers.com.

This analysis is for educational purposes and does not constitute financial or legal advice. ICHRA design involves complex ACA, ERISA, and tax considerations. Consult your benefits advisor for guidance specific to your company structure.

About the Author

Sam Newland, CFP® is the Founder and President of Business Insurance Health and PEO4YOU. Contact: [email protected] | 857-255-9394